Next: Summary of statistical notation

Up: Basic probability concepts

Previous: Odds

Contents

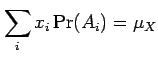

If probabilities are known for all events in event space, it is

possible to calculate the expectation (population mean)

of a random variable

where  is the value taken by the random variable for event

is the value taken by the random variable for event

; i.e.

; i.e.

.

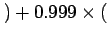

As an example, if there is a one in a thousand chance of

winning a lottery prize of £1500 and each lottery

ticket costs £2 then the expectation (expected long

term profit) is -£0.50=

.

As an example, if there is a one in a thousand chance of

winning a lottery prize of £1500 and each lottery

ticket costs £2 then the expectation (expected long

term profit) is -£0.50=

£(1500-2)

£(1500-2)

-£2

-£2 .

A useful property of expectation is that the expectation of any

linear combination of two random variables

is simply the linear combination of their respective

expecations

.

A useful property of expectation is that the expectation of any

linear combination of two random variables

is simply the linear combination of their respective

expecations

where  and

and  are (non-random) constants. Note also

that

are (non-random) constants. Note also

that

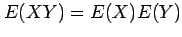

if X and Y are independent random

variables.

if X and Y are independent random

variables.

The expectation can also be used to define the population

variance

which provides a very useful measure of the overall

uncertainty in the random variable.

The variance of a linear combination of two

random variables is given by

where and are (non-random) constants.

The quantity

is known as the

covariance of and

is known as the

covariance of and  and is equal to zero

for independent variables.

The covariance can be expressed as

and is equal to zero

for independent variables.

The covariance can be expressed as

where  is a dimensionless number lying between -1 and 1

known as the correlation between and .

Correlation is widely used to measure the amount of

linear association between two variables.

is a dimensionless number lying between -1 and 1

known as the correlation between and .

Correlation is widely used to measure the amount of

linear association between two variables.

Note that the quantities  and

and  refer

specifically to population parameters and

NOT sample means and variances. To avoid confusion

the sample mean of an observed variable

refer

specifically to population parameters and

NOT sample means and variances. To avoid confusion

the sample mean of an observed variable  is denoted by

is denoted by

and the sample variance is denoted by

and the sample variance is denoted by  .

Sample covariance is denoted

.

Sample covariance is denoted  and sample correlation

is denoted by

and sample correlation

is denoted by  .

These provide estimates of the population quantities but

should never be confused with them !

.

These provide estimates of the population quantities but

should never be confused with them !

Next: Summary of statistical notation

Up: Basic probability concepts

Previous: Odds

Contents

David Stephenson

2005-09-30